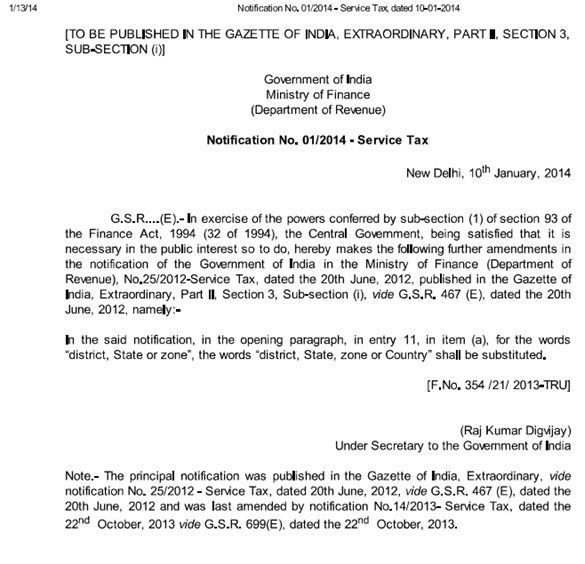

|

II. Direct Tax Case laws:

1. Exotic Fruits (P.)

Ltd. v. Income-tax Officer (International Taxation) Ward -1(1),

Bangalore, IT APPEAL NOS. 1008 TO 1013 (BANG.) OF 2012, Date of Order:

OCTOBER 4, 2013 – ITAT – Banglore.

Where

assessee had paid export commission to its non-resident agent, in view

of fact that services of non-resident agents were rendered outside India

and commission was also paid outside India, income of such agent by way

of commission could not be considered as accrued or arisen or deemed to

be accrued or arisen in India

Assessee's

agents based abroad have never rendered any services in India.

Admittedly, none of the assessee's agents have their offices or business

establishments in India for rendering such services to the assessee.

The commissions to such agents have been paid not in India but overseas.

Since no part of the services were rendered by such agents in India, no

income arose on the payment of commissions to such agents and,

consequently, as rightly argued by the assessee, the question of

deduction of tax at source under section 195 doesn't arise.

(Please click here to view the Judgment)

2. Commissioner Of Income Tax vs. M/S Jogendra Singh &

Company, ITA No. - 1 of 2014, Date of Order : 06.01.2014, Allahabad High

Court.

Whether the ITAT erred in law in deleting the additions made U/s 68

on the basis of affidavits only, ignoring the provisions and spirit and

aim of the legislature

in formulating Section 68.

Held Yes

During

the stage of the remand proceeding, the assessee had filed by way of

affidavits confirmations from the creditors. Subsequently, three

remaining creditors had also filed confirmations. The Tribunal has

compared the same with the list of sundry creditors in the balance-sheet

for the earlier year ending on 31 March 2007. It has been found that

the creditors have provided building material for civil construction

work and road roller and JCB machine for the use of the business

activities of the assessee and, therefore, if some outstanding amount

was left due at the end of the financial year, which was confirmed by

the creditors, this could not be regarded as an unexplained liability.

(Please click here to view the Judgment)

|

{kind=link}

New User?

New User?  Subscribe Now

Subscribe Now